Delving into the world of Tax-Advantaged Income Funds, this overview promises a deep dive into a lucrative investment option that offers both financial growth and tax advantages.

As we explore the intricacies of Tax-Advantaged Income Funds, we uncover the key benefits, risks, and strategies that make them a compelling choice for savvy investors.

Tax-Advantaged Income Funds

Tax-Advantaged Income Funds are investment vehicles that offer income generation while providing tax benefits to investors. These funds typically invest in assets that generate income, such as dividends, interest payments, or capital gains, and are structured in a way to minimize the tax impact on those earnings.

Examples of Tax-Advantaged Income Funds

- Dividend Growth Funds: These funds focus on investing in stocks of companies that have a history of increasing dividends over time. They offer tax-efficient returns due to the qualified dividend tax rate.

- Municipal Bond Funds: These funds invest in municipal bonds issued by state and local governments. The interest income from these bonds is typically exempt from federal taxes and in some cases, from state taxes as well.

Benefits of Investing in Tax-Advantaged Income Funds

- Tax Efficiency: By investing in tax-advantaged income funds, investors can minimize the tax impact on their investment returns, allowing them to keep more of their income.

- Diversification: These funds offer diversification benefits by investing in a variety of income-generating assets, reducing the risk associated with any single investment.

- Steady Income: Tax-advantaged income funds are designed to provide a steady stream of income to investors, making them suitable for those seeking regular cash flow.

Comparison with Traditional Income Funds

- Tax Treatment: Tax-advantaged income funds are structured to minimize the tax impact on investment returns, while traditional income funds may be subject to higher tax rates on dividends and capital gains.

- Income Sources: Tax-advantaged income funds may focus on specific assets or sectors to optimize tax benefits, while traditional income funds may have a broader investment mandate.

- Risk Profile: Tax-advantaged income funds tend to be more conservative in their approach to generate income, focusing on tax-efficient strategies, whereas traditional income funds may take on more risk for potentially higher returns.

Income Funds

Income funds are investment vehicles that primarily focus on generating income for investors rather than capital appreciation. The main objective of income funds is to provide a steady stream of income through dividends, interest payments, or other distributions.

Types of Assets in Income Funds

Income funds typically hold a diversified portfolio of assets such as bonds, dividend-paying stocks, real estate investment trusts (REITs), preferred stocks, and other fixed-income securities. These assets are selected to generate regular income for investors while managing risk.

Potential Risks Associated with Income Funds

While income funds are generally considered less risky than growth-oriented funds, they are still subject to various risks. Some of the potential risks associated with income funds include interest rate risk, credit risk, inflation risk, and market risk. Investors should carefully assess these risks before investing in income funds.

Strategies for Maximizing Returns from Income Funds

To maximize returns from income funds, investors can consider strategies such as diversifying their holdings, reinvesting dividends, and actively managing their portfolio. Additionally, investors can research and select income funds with a track record of consistent income generation and strong performance.

Index Funds

Index funds are a type of mutual fund or exchange-traded fund (ETF) that tracks a specific stock market index, such as the S&P 500. Unlike income funds, which focus on generating regular income, index funds aim to replicate the performance of the underlying index.

Differentiate between income funds and index funds

- Income funds focus on generating regular income through dividends, interest payments, or other distributions, while index funds aim to match the performance of a specific market index.

- Income funds may invest in a variety of securities, including bonds, preferred stocks, or dividend-paying stocks, to generate income, whereas index funds typically hold a diversified portfolio of stocks or bonds that mirror the components of the index they track.

Advantages of investing in index funds

- Low fees: Index funds generally have lower management fees compared to actively managed funds, making them a cost-effective investment option.

- Diversification: By investing in an index fund, investors gain exposure to a broad range of securities, reducing individual stock risk.

- Passive management: Index funds require minimal management since they aim to replicate the performance of a specific index, resulting in lower turnover and tax efficiency.

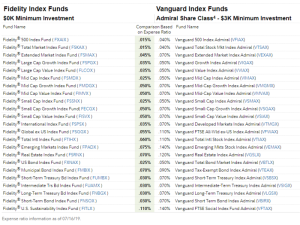

Popular index funds in the market

- Vanguard Total Stock Market Index Fund (VTSAX): Tracks the performance of the CRSP US Total Market Index, providing exposure to the entire U.S. stock market.

- S&P 500 ETFs: Examples include SPDR S&P 500 ETF (SPY) and Vanguard S&P 500 ETF (VOO), which replicate the performance of the S&P 500 index.

Using index funds to build a diversified investment portfolio

- Investing in a mix of index funds that track different asset classes, such as domestic stocks, international stocks, and bonds, can help investors build a diversified investment portfolio.

- By allocating funds across various index funds, investors can spread risk and potentially achieve a more stable return over the long term.

Inflation Hedge

Income funds can serve as an effective hedge against inflation, providing investors with a way to combat the eroding effects of rising prices on their purchasing power. By investing in income funds, individuals can potentially generate a steady stream of income that has the potential to keep pace with or even outpace inflation over time.

Benefits of Using Income Funds as an Inflation Hedge

- Income funds typically consist of a diversified portfolio of income-producing assets such as bonds, dividend-paying stocks, and real estate investment trusts (REITs). These assets have the potential to generate a consistent stream of income regardless of market conditions, helping investors maintain their purchasing power in the face of inflation.

- Some income funds follow a strategy of investing in assets that have historically shown resilience to inflationary pressures. For example, Treasury Inflation-Protected Securities (TIPS) are specifically designed to protect against inflation by adjusting their principal value based on changes in the Consumer Price Index (CPI).

- Dividend-paying stocks are another popular component of income funds that can act as an inflation hedge. Companies that regularly increase their dividends tend to have strong cash flows and the ability to pass on higher costs to consumers, making them less vulnerable to the effects of inflation.

Strategies for Optimizing Income Funds to Combat Inflation

- Consider allocating a portion of your investment portfolio to income funds that have a track record of delivering consistent returns that outpace inflation. Look for funds with a history of dividend growth and capital appreciation.

- Diversification is key when using income funds as an inflation hedge. Spread your investments across different asset classes and sectors to reduce risk and enhance the potential for long-term growth.

- Regularly review and adjust your income fund holdings to ensure they remain aligned with your investment goals and risk tolerance. Rebalancing your portfolio can help you stay ahead of inflation and capitalize on new opportunities in the market.

Insurance Premiums

Investing in tax-advantaged income funds can have a significant impact on managing insurance premiums. By strategically utilizing income funds, individuals can effectively offset insurance costs and potentially enjoy tax benefits in the process.

Offsetting Insurance Costs

- Income generated from tax-advantaged income funds can be used to cover insurance premiums, reducing the out-of-pocket expenses for policyholders.

- By reinvesting the income earned from these funds, individuals can potentially grow their investment over time, providing a sustainable source of funds to pay for insurance.

Tax Implications

- Using income funds to pay insurance premiums may offer tax advantages, as the income generated from these funds may be subject to lower tax rates compared to other forms of income.

- It’s important to consult with a tax professional to understand the specific tax implications of using income funds for insurance payments and to ensure compliance with tax regulations.

Tips for Effective Management

- Regularly review and assess the performance of tax-advantaged income funds to maximize returns and ensure sufficient income to cover insurance costs.

- Consider diversifying investments within income funds to mitigate risks and enhance the stability of income streams for insurance premium payments.

- Stay informed about changes in tax laws and regulations that may impact the tax treatment of income funds used for insurance expenses.

In conclusion, Tax-Advantaged Income Funds emerge as a powerful tool for building wealth while minimizing tax liabilities, making them an attractive option for those seeking financial growth and stability.

User Queries

How do tax-advantaged income funds differ from traditional income funds?

Tax-advantaged income funds offer unique tax benefits that traditional income funds do not, such as tax-free growth or tax-deferred distributions.

Can tax-advantaged income funds help in managing insurance expenses effectively?

Yes, investing in tax-advantaged income funds can provide a source of income that can be used to offset insurance costs, offering a strategic financial advantage.